Leaning against a rusted tailgate in a windy yard in Bridgeport, Connecticut, Devin showed me a spreadsheet that made my stomach turn. He was spending $4,832 a month just on short-term repairs and emergency rentals for three trucks that should have been retired five years ago. Devin is a hell of a roofer, but his "cash is king" philosophy was actually bleeding his business dry. We stood there watching his crew struggle to manually haul bundles up a steep three-story Victorian, a scene that looked more like 1994 than 2024. I asked him how much that bottleneck was costing him in labor hours, and he didn't have an answer.

That is the hidden trap for many contractors across the Northeast. We pride ourselves on being gritty and making things last, but there is a mathematical point where "making it last" becomes a massive financial liability. When you're paying a crew of six to wait around because a lift is down or a truck won't start in the October chill, you aren't saving money by avoiding a monthly payment. You're actually subsidizing the bank's risk with your own inefficiency.

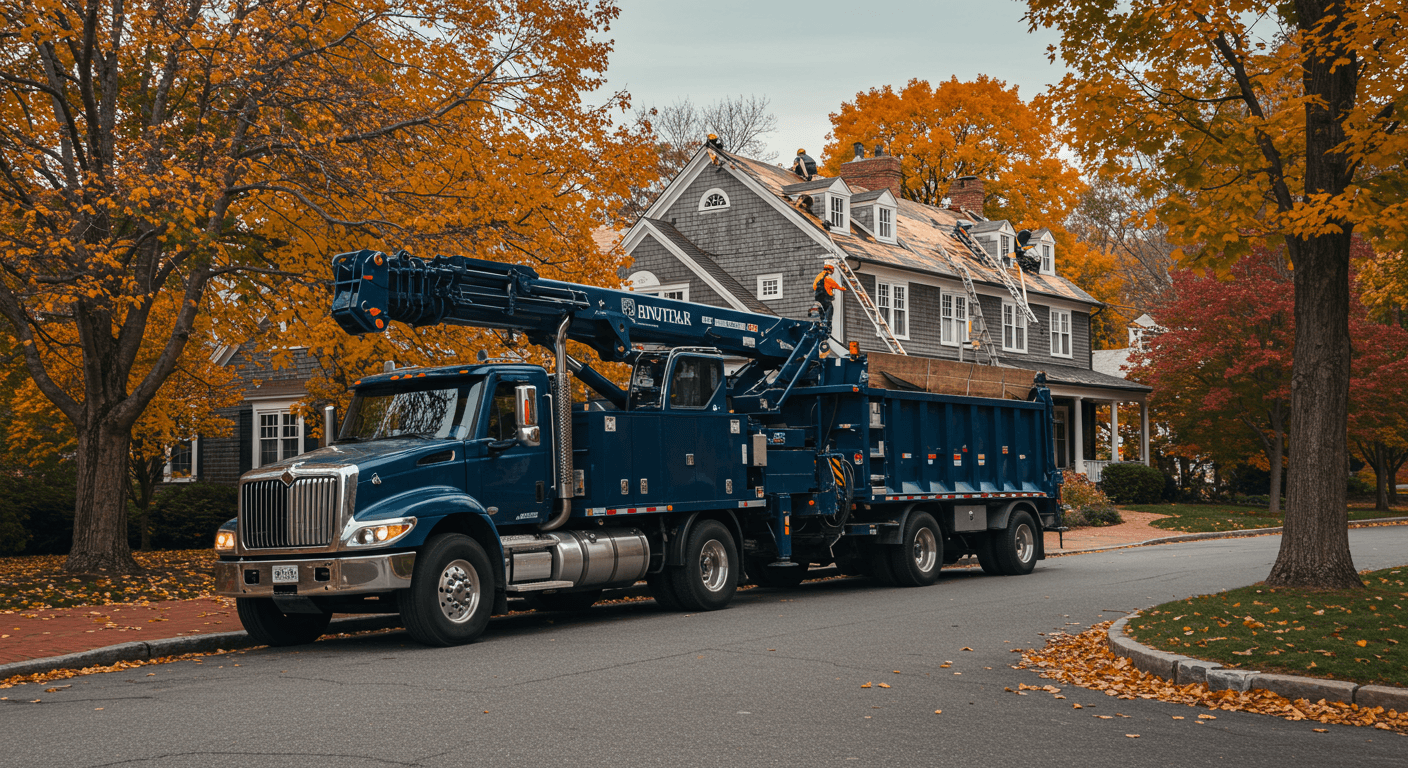

Average monthly revenue lost to equipment downtime and manual labor inefficiencies in mid-sized Northeast roofing firms

At a Glance

Stop viewing financing as "debt" and start viewing it as a tool to lower your effective labor rate.

Leverage Section 179 tax deductions to write off the full purchase price of equipment in the first year.

Use specific ROI calculations to determine if a new piece of equipment will pay for its own monthly note through saved man-hours.

Align your equipment capacity with a reliable stream of job opportunities to ensure the machines never sit idle.

The High Cost of Playing It Safe

I recently coached a shop in Massachusetts that was terrified of taking on a $2,400 monthly payment for a specialized debris management system and a new crane truck. They were convinced that staying debt-free was the "safe" play. However, once we sat down and looked at the data, the reality was startling. Their "safe" approach was costing them $6,740 per month in excess labor, dump fees, and property damage claims from manual shingle teardowns.

In the Northeast, our season is condensed. We don't have the luxury of slow days when the weather turns. If your equipment isn't 100% reliable, you're missing the window to maximize your annual revenue. According to Roofing Contractor Magazine, the move toward specialized equipment is no longer a luxury but a necessity for maintaining competitive margins in high-cost labor markets.

When I talk to owners about this, I often use a specific script to help them reframe the conversation with their partners or spouses. Instead of saying, "I want to buy a new truck," try saying: "I'm looking to trade $5,000 in monthly waste for a $2,200 monthly investment that increases our daily output by two squares."

Financing vs. Cash vs. Leasing

| Metric | Cash Purchase | Strategic Financing |

|---|---|---|

| Cash Flow Impact | High upfront drain | Low monthly payment |

| Tax Advantage | Full immediate deduction | Section 179 eligible |

| Ownership | Immediate ownership | Full ownership at end |

| Maintenance | Owner responsibility | Owner responsibility |

Cash Flow Impact

Tax Advantage

Ownership

Maintenance

Calculating the Real ROI of a Monthly Note

The biggest mistake I see during sales training sessions is when a rep or owner looks at a piece of equipment and only sees the price tag. I was working with a rep named Avery in New Jersey last month who was frustrated because the production team couldn't keep up with his sales volume. The bottleneck? They only had one functional trailer.

We ran the numbers on a new $48,600 dump trailer. With a 6.4% interest rate over 48 months, the payment was roughly $1,150. By adding that trailer, Avery's crew could finish jobs 4.5 hours faster by eliminating the double-handling of debris. If that crew costs $180 per hour in burdened labor, the trailer pays for its entire monthly note in just two jobs. Everything after that is pure profit.

The 3X Rule for Equipment

"Before signing a financing agreement, ensure the equipment will either save or generate 3X its monthly payment in labor hours or increased production capacity. If a $1,200 payment doesn't save you $3,600 in labor or add $3,600 in margin, reconsider the purchase."

Navigating the Northeast Lending Environment

Financing in our region can be tricky because of the seasonal nature of the work. Many traditional banks don't understand the "winter dip" that occurs in places like upstate New York or Maine. This is why I always recommend working with lenders who specialize in the trades. They are more likely to offer flexible payment structures, such as "skip-payment" programs where you pay less during January and February and more during the peak summer months.

The Western States Roofing Contractors Association often highlights that regional economic shifts require contractors to be more agile with their capital. Even if you aren't in the West, their resources on equipment lifecycles are invaluable for any owner trying to decide when to pivot from repair to replacement.

Action Plan

How to conduct an Equipment ROI Audit before financing

A systematic approach to evaluating whether equipment financing makes financial sense for your roofing operation.

Track Downtime: Log every hour a crew sits idle due to equipment failure or lack of tools over a 30-day period.

Calculate Burdened Labor: Determine your true cost per hour for a full crew (wages, taxes, insurance).

Identify the Bottleneck: Is it transportation, material lifting, or debris removal?

Quote the Solution: Get a firm monthly payment quote for the specific equipment that solves that bottleneck.

Compare Costs: If (Downtime Hours x Labor Rate) > Monthly Payment, financing is the mathematically correct decision.

Want to skip the manual work and get exclusive, verified leads instead?

Get $150 in Free CreditsWhy Leads and Equipment Go Hand-in-Hand

There is no point in financing a $75,000 rig if it's going to sit in your driveway. I've seen shops get into trouble when they scale their equipment capacity but forget to scale their lead flow. When you take on a new monthly obligation, your "break-even" point moves. You need to ensure your sales team is fed with high-quality opportunities to keep those new wheels turning.

I've seen shops transform their pipeline by securing exclusive, verified leads that allow them to plan their production schedule weeks in advance. If you know exactly what your next six weeks look like, taking on a financing note feels much less like a gamble and much more like a calculated expansion. You can even manage these new opportunities on the fly using a dedicated mobile app to ensure your new equipment is never sitting idle while you're out in the field.

The Balloon Payment Trap

Avoid financing deals with low initial payments that end in a massive "balloon" payment. In the roofing industry, equipment takes a beating. You don't want to owe a $15,000 lump sum on a truck that has 150,000 hard miles on it four years from now.

The Psychological Shift of the Top 1%

The most successful contractors I coach in Philadelphia and Boston don't brag about their "paid-for" junkers. They brag about their uptime. They understand that their most valuable asset isn't the truck, it's the 10 hours of sunlight their crew has to work with.

When you finance strategically, you aren't just buying a machine. You are buying back time. You are buying your crew's morale (no one wants to work for the guy with the truck that breaks down on the I-95 every Tuesday). And most importantly, you are buying the ability to say "yes" to bigger, more profitable jobs that your old equipment simply couldn't handle.

If you're ready to scale your operation with the right equipment and a reliable stream of job opportunities, the math becomes clear. The question isn't whether you can afford the monthly payment. It's whether you can afford to keep losing money to inefficiency.