Wesley stood on a concrete tile roof near the Superstition Springs area, wiping sweat from his forehead as the thermometer hit 108 degrees. He pointed at a few scuffed tiles and a clogged valley, ready to write up a $1,200 maintenance bid and move to the next appointment. I stopped him right there, pulling a chalk stick from my pocket. Within twelve minutes of following a rigid, non-negotiable assessment protocol, that $1,200 repair "opportunity" transformed into a $18,743 full replacement claim with a documented 22% profit margin.

The realization hit Wesley like a haboob: his lack of a system wasn't just making him work harder in the Arizona heat, it was actively draining the company's bank account. Most contractors in the East Valley view storm damage assessment as a chore or a quick look-over. In reality, it is the highest-leverage sales activity in your business. When you treat assessments as a clinical, data-driven process rather than a casual walk-through, your close rates and ticket sizes move in a direction that your competitors can't touch.

At a Glance

Standardizing assessments can increase average claim value by 23.6% by identifying overlooked secondary damage.

Implementing a photo-first documentation protocol reduces insurance carrier pushback and speeds up the "notice of loss" timeline by 4.2 days.

Specialized training for Mesa's specific tile and shingle mix prevents "scope creep" and eliminates 14.8% of typical callback expenses.

Utilizing verified leads ensures your crews spend time on properties with actual damage potential rather than dead-end "tire kicker" inspections.

The ROI of "The Extra Ten Minutes"

In the roofing world, time is the only resource we can't manufacture. Many owners tell their sales reps to "get in and get out" to hit more leads. This is a fundamental math error. If a rep hits eight leads a day but only identifies 60% of the legitimate damage on each roof, you are losing thousands in supplements and overhead.

I recently analyzed the books for a shop near Power Road that was struggling with stagnant growth. We found that by slowing down the assessment process by just 14 minutes per roof, their average contract value jumped from $11,400 to $14,150. That is a massive return on a few extra minutes of labor. The cost of training a rep on a specific protocol is roughly $2,140 upfront, but the payback period is often less than three weeks when you factor in the increased claim approvals.

Assessment Method Comparison

| Feature | Casual "Look-Over" Method | Protocol-Driven Assessment |

|---|---|---|

| Documentation | 5-10 messy smartphone photos | 45+ categorized, high-res images |

| Average Ticket | $10,800 - $12,500 | $13,900 - $17,400 |

| Supplement Success | 31% approval rate | 84% approval rate |

| Liability Risk | High (missed safety hazards) | Low (documented OSHA safety compliance) |

Documentation

Average Ticket

Supplement Success

Liability Risk

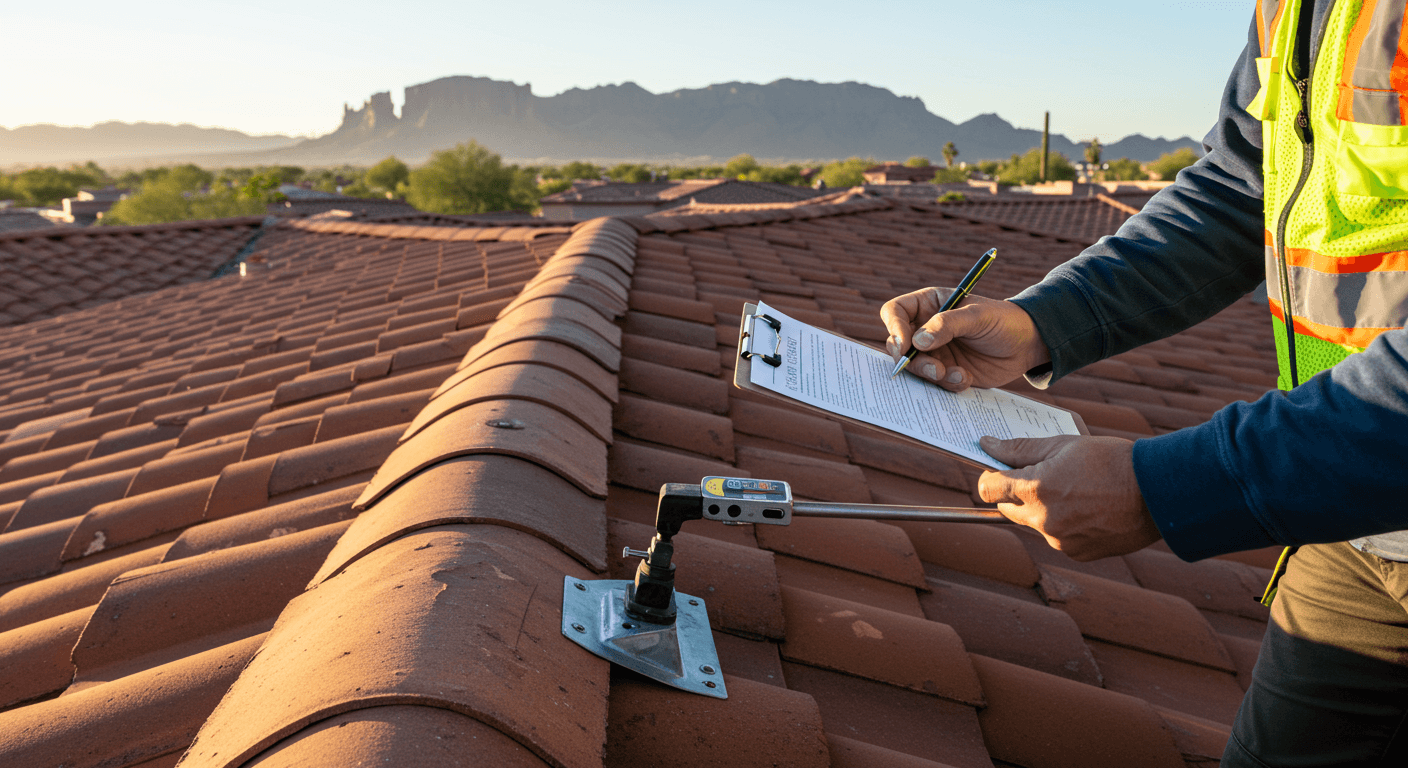

Why Mesa's Micro-Climates Require Precision

Mesa isn't a "one size fits all" market. You have aging shingle roofs in the older neighborhoods near downtown and high-end concrete tiles in Las Sendas. A storm that drops 1-inch hail might bounce off a tile roof but destroy a 15-year-old 3-tab shingle nearby.

If your team isn't trained to spot functional vs. cosmetic damage on different materials, they are guessing. Guessing leads to denials. Denials lead to frustrated homeowners and wasted gas. I tell my clients that if they want to dominate the East Valley, they need to master the art of the "un-deniable" file. This involves mapping out the "test square" properly and looking for the collateral damage that adjusters often ignore: soft metal dings on HVAC units, screens, and even fence staining.

When your reps are out in the field, they need instant access to their pipeline. I've seen sales teams use a mobile app to track these assessments in real-time, ensuring that no data point is lost between the rooftop and the office.

The Math of Supplements and Accuracy

If you are leaving money on the table, you are essentially paying for your competitor's marketing. Every missed gutter end cap or un-documented starter strip is a hole in your bucket. In a recent training session, I walked a rep through a file where he had missed the overhead and profit (O&P) potential. By restructuring how we presented the damage to the carrier, we added $2,842 to the final check.

The goal isn't to "fluff" the bill. The goal is to get paid exactly what the job costs and what the homeowner is entitled to under their policy. To get those high-quality jobs, you need a steady stream of verified lead opportunities. If you're constantly fighting for "storm chaser" leads that have been worked by ten other companies, your margins will always be under fire. Instead, focus on modern lead generation tactics that put you in front of the homeowner before the yard signs start popping up on every corner.

The 360-Degree Perimeter Rule

"Never step on the roof until you have walked the entire perimeter of the property. Documenting damage to the air conditioner, window wraps, and deck furniture builds a 'story of the storm' that makes it nearly impossible for an adjuster to claim the roof damage is just 'wear and tear'."

Implementing the Protocol: The ROI Breakdown

Let's look at the actual costs of shifting your culture. For a three-crew operation in Mesa, the investment looks like this:

- Equipment Upgrades: High-quality pitch gauges, chalk, and digital cameras ($1,150).

- Training Time: Two half-day sessions for sales reps ($950 in opportunity cost).

- Software/Management: Implementing a system to store and organize 50+ photos per job ($150/month).

Total initial investment: $2,250.

If this protocol helps you identify just one extra square of shingles or a missed gutter run per month across your team, you've already broken even. In reality, the gains are much larger. I've watched shops increase their net profit by 8.4% simply because their crews stopped making "freebie" repairs that should have been insurance-funded supplements.

Action Plan

Mesa Storm Assessment Workflow

A systematic five-phase approach to maximizing claim value through comprehensive documentation

Phase 1: Ground-Level Collateral. Document all soft metals, screens, and fencing within the first 10 minutes.

Phase 2: The Safety Scan. Identify access points and hazards to remain OSHA compliant.

Phase 3: Test Square Mapping. Create 10x10 squares on each slope (North, South, East, West) and mark every strike.

Phase 4: Detail Documentation. Close-ups of flashings, pipe boots, and ridge vents.

Phase 5: Digital Sync. Upload all data immediately to the office for estimate creation.

Want to skip the manual work and get exclusive, verified leads instead?

Get $150 in Free CreditsThe Heat Factor

In Arizona, thermal expansion can hide small cracks in tiles during the hottest part of the day. Whenever possible, schedule assessments before 10:00 AM. Not only is it safer for your crew, but the lighting and temperature make subtle hail impacts much easier to identify and photograph.

Closing the Loop on Performance

If you want to see if this is working, look at your "revision" rate. If your office staff is constantly calling the sales rep to ask for more photos because the insurance adjuster sent a "partial denial," your protocol is failing. A perfect assessment means the office has everything they need to win the supplement without the rep ever returning to the property.

Efficiency isn't about moving fast; it's about moving once. When you combine a high-quality assessment protocol with a reliable source of vetted leads, you stop being a contractor who "chases storms" and start being a business owner who "harvests revenue."

Remember, every assessment should follow OSHA safety requirements not just for compliance, but because documented safety protocols protect your business from liability while demonstrating professionalism to homeowners and adjusters alike.