Conventional wisdom tells you that paying cash for a new dump trailer or a shingle lift is the hallmark of a stable, successful roofing business. We have all heard the old-timers in the Georgia roofing scene preach that if you cannot buy it outright, you cannot afford it. This mindset feels safe, especially when you are navigating the unpredictable storm seasons in the Lowcountry, but it is a fundamental misunderstanding of how modern capital works. Relying solely on cash reserves to fund your fleet is not a badge of honor; it is often a silent anchor that prevents you from grabbing the market share currently up for grabs in fast-growing areas like Pooler or Richmond Hill.

At a Glance

Preservation of working capital for emergency marketing or material price spikes.

Direct tax advantages through Section 179 that often exceed the first year of interest payments.

Improved crew retention by providing reliable, modern tools that reduce physical strain.

Enhanced brand authority in premium Savannah neighborhoods through professional-grade appearances.

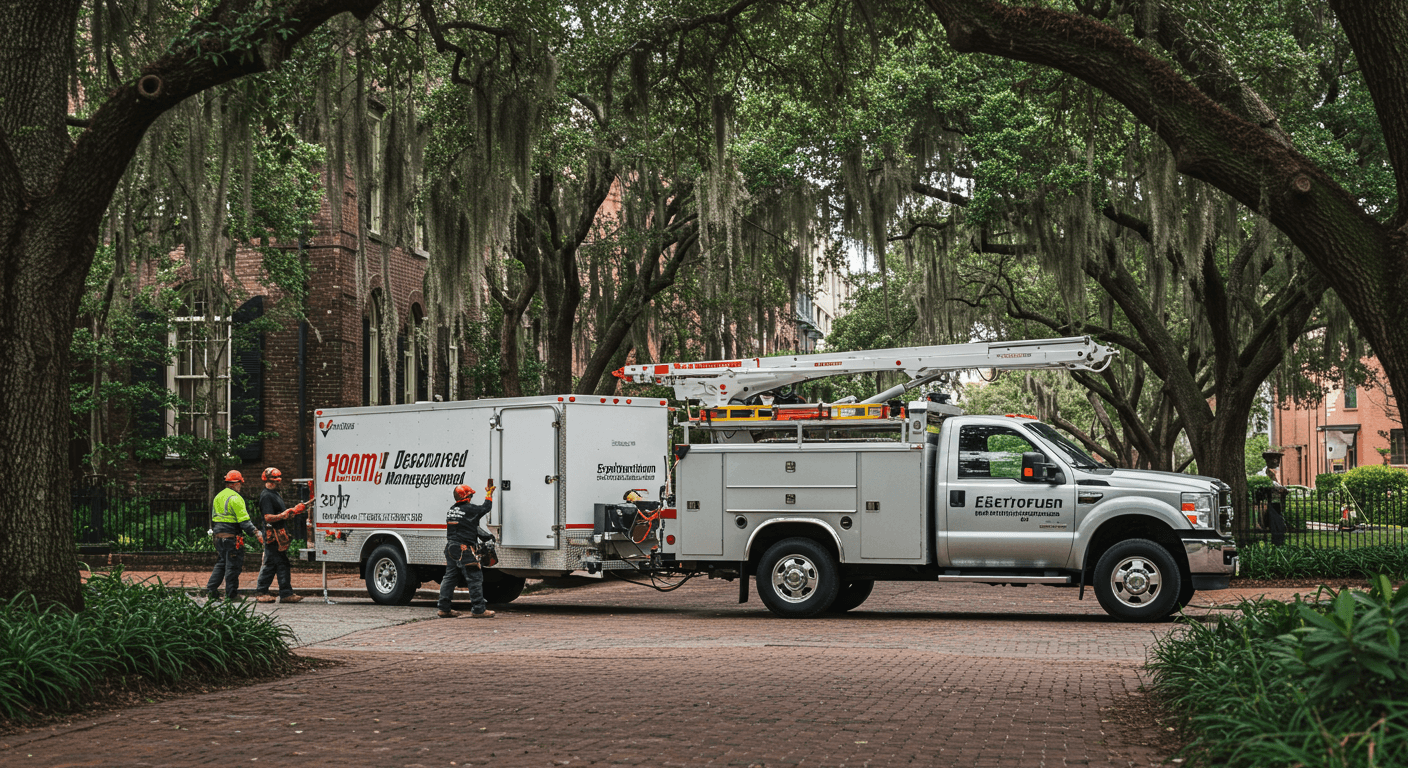

I was standing in a dusty lot off Dean Forest Road recently with a contractor named Jaxon. He was staring at a 2017 truck that had just vomited its transmission for the third time in 14 months. Jaxon is a meticulous guy, the kind who knows his margins down to the penny, yet he was terrified of a $1,450 monthly payment for a new rig. He had $52,300 sitting in a high-yield savings account, feeling "protected," while his crew sat idle for two days waiting for a rental. That "protected" cash was actually costing him $3,800 in lost labor and delayed project milestones. We sat down and looked at the actual math of leverage, and the reality was jarring. By refusing to finance, he was essentially paying a 24% "inefficiency tax" just to avoid a 6.7% interest rate.

The myth that debt is always dangerous ignores the reality of inflation and the time value of money. In a high-humidity environment like Savannah, where salt air near Thunderbolt and the islands eats through trailer frames and hydraulic lines faster than in inland Georgia, equipment reliability is a direct contributor to your bottom line. If you are waiting until you have the full $84,600 for a new specialized debris manager, you are missing out on the 18.3% lift in job site speed that equipment provides today.

The Invisible Cost of the "Good Enough" Fleet

When Jaxon finally looked at his numbers, the breakthrough did not come from a spreadsheet. It came from realizing that his "good enough" equipment was destroying his reputation with the high-end homeowners in the Landings and Dutch Island. Modern roofing is as much about the "show" of professionalism as it is about the shingles. A leaking oil pan on a client's pristine pavers is a $2,500 cleanup bill and a one-star review that costs you ten times that in future leads.

The Savannah market is unique because of our geography. We have narrow, oak-lined streets downtown where a massive, outdated dump truck is a liability, not an asset. Financing allows you to pivot into specialized, nimble equipment like compact telehandlers or smaller, high-capacity trailers that allow your crews to get in and out of tight historic districts 22% faster. According to the National Roofing Contractors Association (NRCA), maintaining a modern fleet is also a primary factor in workforce retention. High-quality crews do not want to work for a shop where the tools break down every Tuesday.

I have seen shops in the Chatham County area struggle to keep their best foremen because the equipment was frustrating to use. If you are asking a crew to manually haul bundles up a ladder because you do not want to finance a power hoist, you are going to lose those men to the guy down the street who sees equipment as a recruiting tool. The cost of turnover for a single skilled lead is roughly $7,400 when you factor in training and lost productivity. That alone covers several months of a financing note.

Decoding the Section 179 Advantage in Georgia

One of the most frequent conversations I have in the field involves the IRS Section 179 deduction. Many contractors treat it like a "maybe" or something only for the big players. In reality, it is a tool designed specifically for the mid-sized shop trying to scale. For a roofing business in Savannah, this can be the difference between a profitable year and a stagnant one.

Let us look at a real scenario. If you purchase a piece of equipment for $62,500 and use the Section 179 deduction, you can often write off the entire purchase price in the first year. If you are in a 22% tax bracket, that is a $13,750 reduction in your tax liability. If your total financing payments for that year were only $9,200, the government essentially paid you to upgrade your fleet. This is the "secret" that the largest roofing franchises use to keep their equipment looking brand new while smaller shops struggle with rust and repairs.

I recently worked with a shop owner who was hesitant about the 7.2% interest rate on a new crane truck. After we mapped out the tax savings and the fact that he could now take on three additional commercial jobs in Garden City that required that specific reach, the "cost" of the loan vanished. We calculated that the truck would pay for itself in 14.3 months, but the tax break provided an immediate cash infusion that he used to bolster his marketing budget.

If you are curious about how other successful owners have navigated these growth hurdles, the LeadZik blog features several deep dives into balancing operational costs with aggressive scaling strategies. The goal is to move from a mindset of "cost" to a mindset of "yield."

Variable Rate Risk

Avoid "Variable Rate" financing agreements in the current economic climate. While the initial rate might look 1.5% lower than a fixed-rate option, a sudden shift in the federal funds rate can turn a manageable $1,100 payment into a $1,650 burden overnight, choking your cash flow when you need it most.

Renting vs. Leasing vs. Buying: The Savannah Decision Matrix

In the Savannah metro area, your decision to lease or buy often depends on the specific type of work you are targeting. If you are focusing on the historic renovations in the Starland District, you might need highly specialized equipment that you only use 35% of the year. In that case, a short-term lease or a rental agreement might make sense. However, for your core fleet, the math almost always favors financing toward ownership.

Leasing is often marketed as the "lower payment" option, but you have to look at the residual value. A well-maintained roofing truck in Georgia holds its value surprisingly well. If you lease for four years and walk away with nothing, you have missed out on the equity that could have been a down payment for your next three vehicles. I generally advise my clients to finance via an EFA (Equipment Finance Agreement) so they own the asset from day one and can take full advantage of the depreciation schedules.

Data from Roofing Contractor Magazine suggests that contractors who own their core equipment have a 12.6% higher enterprise value when they eventually look to sell their business. Financing allows you to build that equity using the bank's money while keeping your cash liquid for things that banks won't finance, like a sudden opportunity to buy a competitor's lead list or an unexpected bulk buy on shingles before a price increase.

The Opportunity Cost of Trapped Capital

The biggest mistake I see Savannah roofers make is tying up $50,000 in a piece of equipment when that same $50,000 could generate a 400% return if spent on high-quality customer acquisition. If you put $50,000 into a truck, you have a truck. If you put $10,000 down on that truck and put the remaining $40,000 into a verified lead pipeline, you have a truck and $200,000 in new contract revenue.

This is where the synergy between financial strategy and lead generation becomes critical. You need the equipment to do the work, but you need the work to pay for the equipment. I have seen contractors get "equipment rich and cash poor," where they have a beautiful fleet sitting in the yard because they spent their entire marketing budget on down payments.

Our team at LeadZik was actually founded by roofers who were tired of seeing this exact cycle of wasted spend and trapped capital. They realized that if you have a reliable way to preview and claim exclusive leads, the "risk" of a monthly equipment payment disappears because the revenue is predictable. When you know exactly how many jobs are available in Savannah next week, a $1,200 truck payment feels like a minor line item rather than a source of anxiety.

Building Your 48-Month Fleet Roadmap

Don't buy equipment as a reaction to a breakdown. That is when you make desperate, expensive decisions. Instead, build a rolling 48-month roadmap. In the Savannah climate, you should assume a shorter lifecycle for certain components due to the heat and salt.

Action Plan

The 48-Month Fleet Roadmap

A strategic approach to equipment planning that prevents reactive purchases and maximizes tax benefits while maintaining operational flexibility.

Audit your current repair costs: If a vehicle is costing you more than $450 a month in non-routine maintenance, it is already more expensive than a new financed replacement.

Project your capacity: If you added one more crew tomorrow, what is the specific equipment bottleneck? Finance that bottleneck before you actually hire the crew.

Consult your tax pro in Q3: Do not wait until December 15th to buy equipment for the tax break. By then, the inventory at the dealers in Garden City and Savannah will be picked over, and you will pay a premium.

Diversify your lenders: Don't just go to your primary bank. Specialized equipment lenders understand the resale value of a roofing rig better than a general commercial bank and will often give you better terms.

Want to skip the manual work and get exclusive, verified leads instead?

Get $150 in Free CreditsIf you are still on the fence about whether your business can handle the overhead of a new fleet, check our FAQ section to see how our lead verification process ensures you have the consistent volume needed to stay cash-flow positive.

Managing a roofing company in a competitive market like Savannah requires more than just knowing how to nail a shingle. It requires a sophisticated approach to your balance sheet. By moving away from the "cash-only" mindset and embracing strategic financing, you free up the capital necessary to dominate the local market. Jaxon eventually pulled the trigger on that new truck, financed at 6.8%. Within three months, his crew's morale was up, his "breakdown" days dropped to zero, and he used his saved cash to launch a targeted campaign in Wilmington Island that brought in $114,300 in new business. That is the power of leverage when it is used correctly.