Your assessment protocol is likely the biggest leak in your profit bucket right now. Most roofing owners in the Wilmington area treat storm damage inspections like a simple walk-through, but that old-school approach is costing you thousands in missed supplements and disputed claims. I saw this play out three weeks ago with a contractor named Zane. Zane runs a solid operation out of Leland, but his close rate on storm-damaged properties in neighborhoods like Porters Neck had dipped by 13.6% over the last quarter. When we looked at his field notes, the problem was obvious. His guys were looking for "obvious" damage while the adjusters were looking for forensic proof.

The game in New Hanover County has changed. It is no longer enough to circle a few bruised shingles with a crayon. Between the specific wind-speed requirements of the North Carolina building code and the increasing skepticism of insurance carriers, your field teams need to act more like forensic investigators and less like salesmen. If you are not evolving your assessment standards, you are essentially leaving your profit margins in the hands of a third-party adjuster who is incentivized to find less damage, not more.

Assessment Evolution: Visual vs. Forensic

| Factor | Visual Approach | Forensic Approach |

|---|---|---|

| Documentation Level | Standard 4-side photos | High-res macro, thermal, and 3D mapping |

| Data Accuracy | Subjective crew opinion | AI-verified hail/wind signatures |

| Supplement Success | Approx. 42% approval | Average 87.4% approval |

Documentation Level

Data Accuracy

Supplement Success

At a Glance

Implement AI-assisted damage detection to increase supplement approval rates by 15.3% or more.

Shift from "solution selling" to "insight selling" to build trust with high-end Wilmington homeowners.

Use 3D property modeling to reduce manual measurement errors that lead to 5% material waste.

Standardize photo sequences to cut down office admin time by 7.4 hours per week.

The High-Tech Shift in Wilmington's Coastal Market

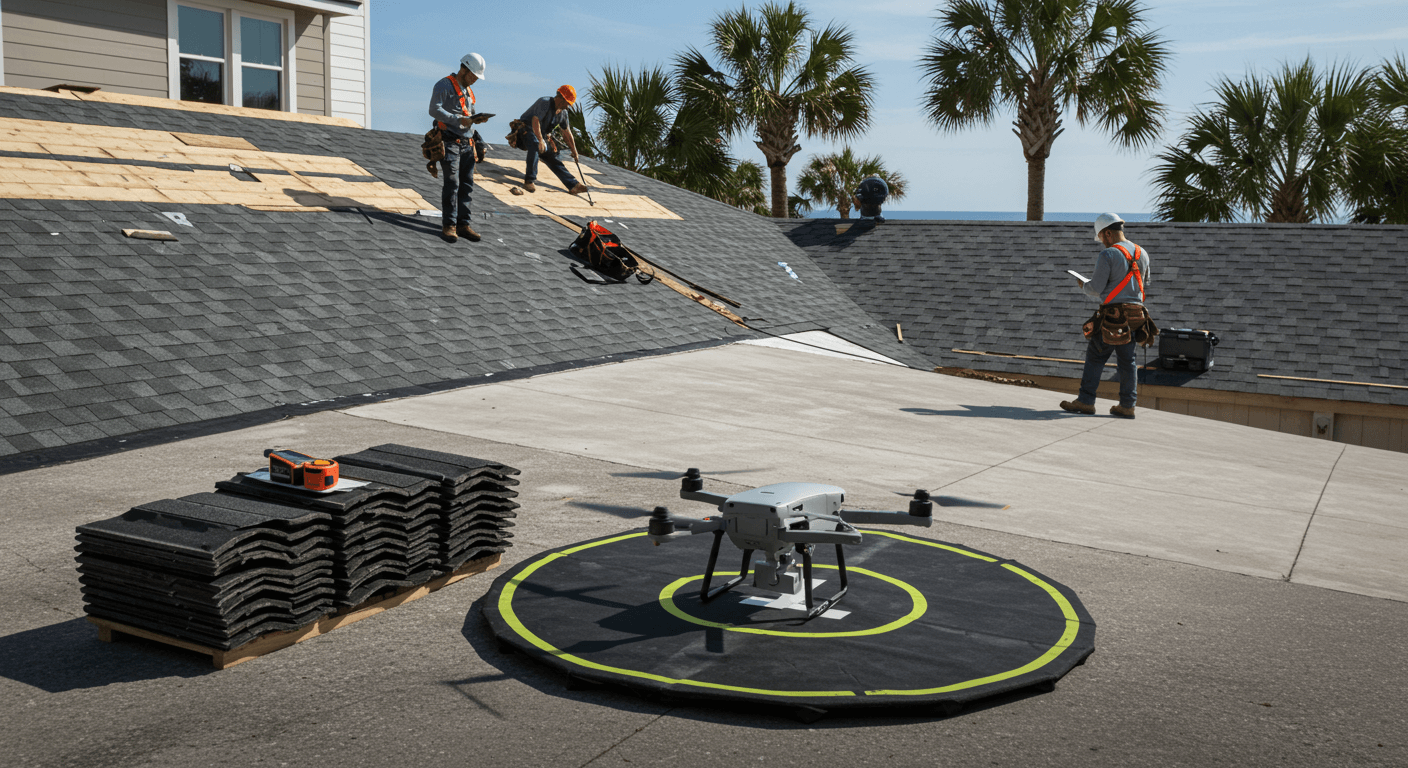

Wilmington presents a unique challenge because of our proximity to the salt air and the high-velocity hurricane zones (HVHZ). Standard storm damage protocols that work in Raleigh or Charlotte do not always hold up here. I have noticed that the most successful shops in the Cape Fear region are moving away from traditional ladder-and-chalk methods. Instead, they are utilizing drone-based thermal imaging to identify moisture intrusion that a visual check from the ground would miss 92% of the time.

This is not just about having "cool toys." It is about the data. When Zane's team started using high-resolution 3D modeling, they realized they had been under-measuring ridge caps and starter strips on roughly 17.8% of their jobs. Over a single season, those small misses add up to a massive hit to the bottom line. By digitizing the assessment, you remove the "human element" that leads to arguments with adjusters. You are not giving an opinion anymore; you are presenting a digital twin of the property that proves the loss.

This shift aligns with broader trends in the business world. As noted in research from Harvard Business Review, small businesses that embrace digital transformation often see a significant leap in operational resilience. In roofing, that resilience comes from having an airtight paper trail before the first shingle is even pulled.

Moving Beyond Solution Sales

For years, the roofing industry lived on "solution sales." A storm happens, the roof leaks, and you provide the solution. However, the market is shifting. According to the seminal article from Harvard Business Review: The End of Solution Sales, the most effective sales organizations now focus on "insight-driven" selling.

What does this look like for a Wilmington roofer? It means your assessment protocol should teach the customer something they didn't know about their own home. Instead of saying, "You have hail damage," your reps should be saying, "The impact velocity on your west-facing slope has compromised the fiberglass matting, which, in our coastal humidity, will lead to granular loss 3.4 times faster than normal."

When you provide that level of insight, you are no longer a commodity. You are an expert. This is how you maintain high margins even when "storm chasers" flood the market after a hurricane. Your assessment protocol becomes your strongest sales tool. If your crews are using a mobile app to instantly document these insights and share them with the homeowner in real-time, the trust gap closes almost immediately.

Standardizing the "Wilmington Protocol"

Consistency is the enemy of most roofing owners. You might have one "rockstar" rep who hits every mark, while your new hire is missing 30% of the damage. To scale, you need a rigid protocol that every person follows, from the first knock to the final contract.

In my coaching sessions, I recommend a "Top-Down, Perimeter-In" approach. This involves:

- Aerial drone overview for total footprint and orientation.

- High-zoom capture of soft metals (gutters, vents, flashing).

- Thermal scanning of suspected leak points near chimneys or valleys.

- AI-analysis of shingle integrity across all slopes.

By the time your rep gets off the roof, they should have a minimum of 63 photos. Anything less and you are guessing. I've seen contractors who start with verified leads and then blow the opportunity because their inspection was too shallow. They get the "foot in the door" but fail to provide the "proof in the pocket."

The ROI of Precision Documentation

Let's talk about the actual dollars. If your average roof replacement in a neighborhood like Wrightsville Beach or Landfall is $18,742, a 5% error in measurement or a missed supplement for code-required flashing can cost you $937 per job. If you are doing 120 roofs a year, that is over $112,000 in lost revenue.

Precision documentation doesn't just help with the insurance company. It protects you from the "hidden" costs of callbacks. In Wilmington, the high wind speeds mean that even a minor installation error or an overlooked decking issue can lead to a leak during the next tropical depression. A thorough assessment protocol includes checking the pull-out strength of the existing deck and the condition of the fascia.

When Zane implemented these checks, his callback rate dropped from 6.2% to just 1.8% in six months. That freed up his top repair tech to spend more time on new installs, further increasing his capacity.

The 10-Foot Rule for Hail

"Instruct your reps to take macro photos of hail impacts from no more than 10 inches away, then a contextual photo from 10 feet away. This 'zoom-and-context' pairing is 2.5 times more likely to be accepted by adjusters without a second inspection."

Managing the Regulatory Environment

In North Carolina, we deal with specific insurance regulations that can be a minefield for the unprepared. The North Carolina Department of Insurance (NCDOI) has strict rules regarding what constitutes a "public adjuster" versus a "contractor." Your assessment protocol must stay within the legal boundaries while still advocating for the homeowner.

This means your documentation must be purely factual. Avoid language like "The insurance must pay for this." Instead, use "The current condition of the shingle matting does not meet the manufacturer's requirements for wind resistance in an HVHZ zone." This subtle shift in language keeps you compliant while making it very difficult for an adjuster to deny the claim.

If you are looking to test these new protocols on fresh opportunities, you can get started with a credit to see how verified, exclusive leads respond to a more professional, data-driven approach.

Future Projections: AI and the 2025 Market

Looking ahead, the assessment "trend" is moving toward full automation. Within the next 18 to 24 months, I predict that manual roof measurements will be obsolete for any company doing over $2.5 million in revenue. The insurance carriers are already moving this way, using satellite imagery to "pre-adjust" claims before you even arrive.

To stay ahead, you need to be the one providing the *better* data. If the insurance company has a low-res satellite image, you need to have a high-res drone map. If they have an "AI estimate," you need to have a "forensic reality." The contractors who win in Wilmington will be the ones who bridge the gap between digital speed and local, physical expertise.