Deciding whether to pivot your crews toward high-ticket TPO work or stay glued to residential shingle volume is a math problem that rattles shops right around $4.8M in yearly revenue. You are weighing fast retail cash cycles against thicker tickets that tolerate longer underwriting and documentation.

The shift is not a sales gimmick alone. Your dispatch board, estimating templates, lien waivers, and safety packets all need parallel tracks before you chase bond-heavy warehouses from the Chicago suburbs out through the Illinois River valley.

Owners who underestimate the payout stretch (some industrial schedules push near 115 days on large draws) routinely starve the retail arm that financed the leap. This playbook is the phased transition I steer shops through so Illinois commercial bids do not eat the liquidity that residential still depends on.

Retail crews anchored to fourteen-day swings get ambushed when retainage and approvals park six figures off the ledger for a quarter.

Commercial Scaling Essentials

Model milestone deposits and retainage pulls early so commercial timelines do not starve payroll built for fourteen-day swings.

Bench-test competencies on low-slope membranes, parapet flashing, and welds before staking production hours on bonded specs.

Split estimating teams so overhead, bond fees, crane logic, and document control pick up roughly twelve points more load than residential retail.

Line up Unlimited licensing and municipal bonding language before you chase public or institutional bid lists.

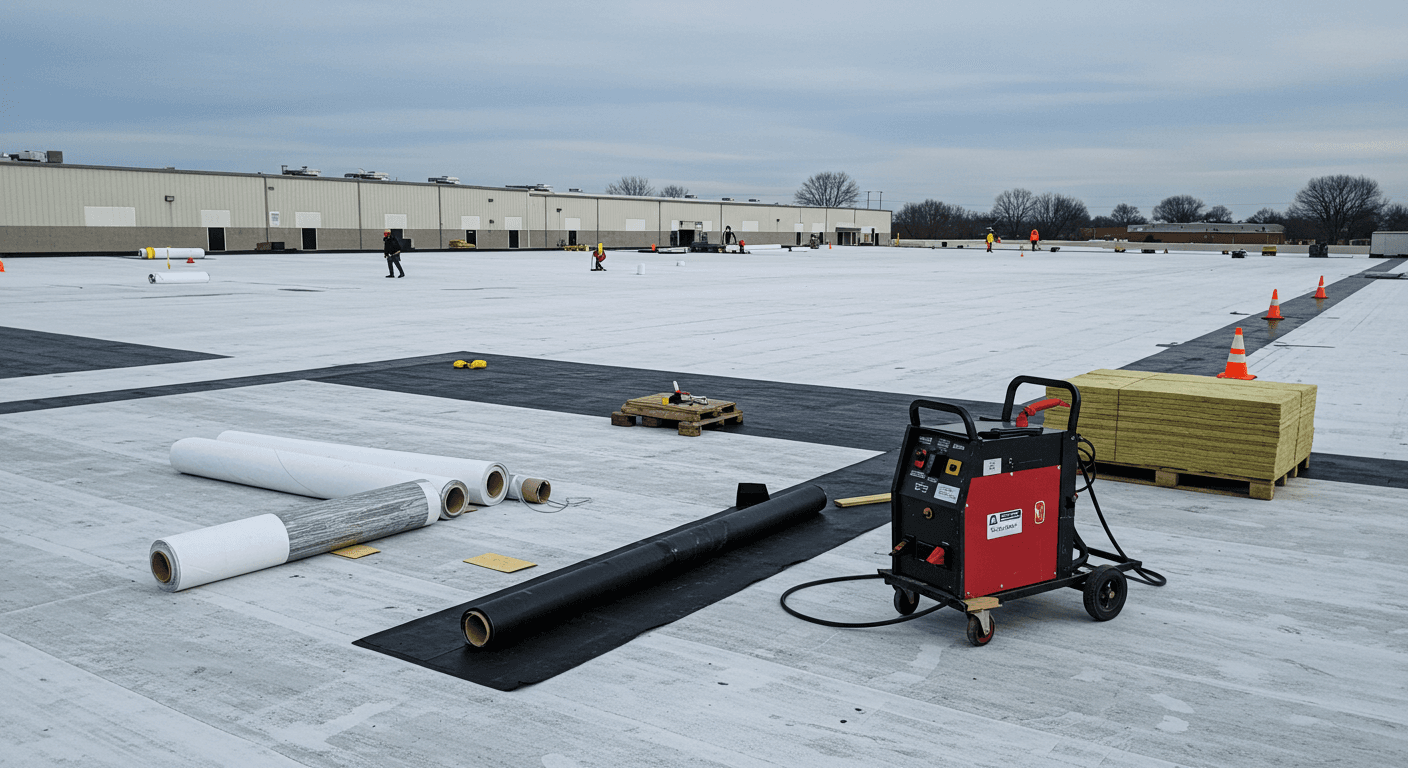

The oversized roof is not oversized residential

Margins that look heroic on spreadsheets can crater once retainage and field learning curves land.

Owners across Naperville, Joliet, and similar commuter markets often imagine commercial roofs as shingles stretched wide. You price a sixty-thousand-square-foot slab with asphalt assumptions and congratulate yourself until the billing calendar disagrees with your bank reconciliation. Retail replacements move: deposit, tear-off, install, collect within fourteen to twenty-one days alongside supplements you already understand.

Sizing the cube footage is not sizing the paperwork

If you mentally convert warehouse square footage into residential squares without rebuilding cash timing, liquidity stress shows up faster than weld crews do.

Inside Illinois, IDFPR expectations and payer-side controls change the soundtrack. Expect retainage hovering near ten percent trapped until punch lists clear and owners release funds sometimes half a year later. When I sift campaign history for crews attempting the crossover, paperwork and compliance hours jump about eighteen percent before anybody adds weld hours. You suddenly own submittal packages and safety narratives that need to line up with technical standards from the National Roofing Contractors Association, plus certified payroll whenever prevailing wage shows up on the bid form.

A contractor outside Aurora ran about $3.2M yearly on disciplined retail work, then signed an $842,000 flat retrofit for a distribution pad. Modeled margin read 24.3% until cranes, parapet pacing, welding rentals, retainage delays, and a residential-trained crew drifting sixteen percent slower on parapet flashing dragged realized net closer to six percent. Three quick retail replacements likely would have banked steadier profit with less reputational jeopardy.

Residential Retail vs Commercial Pipelines

| Metric | Residential retail | Commercial / industrial |

|---|---|---|

| Cash rhythm | High velocity (often 14 to 21 days) | Slower pulls (often 60 to 120 days) |

| Sales cycle | Short (often 1 to 7 days) | Long (often 3 to 12 months) |

| Crew specialization | Steep slope / laminated asphalt | Low slope / weldable membranes / structural metal |

| Lead source emphasis | Homeowner direct | Facilities, owners reps, landlords, capital plans |

| Risk posture | High volume, moderate liability envelopes | Lower volume spans with sharper liability tails |

Cash rhythm

Sales cycle

Crew specialization

Lead source emphasis

Risk posture

Action Plan

Operational split before you sprint the bid boards

You cannot responsibly run bonded industrial work inside the same daily cadence as a twelve-thousand-dollar retail replacement. Separate how you chase, qualify, estimate, mobilize, and cash each lane.

Rebuild cash forecasting using milestone approvals, retainage haircuts, and union or prevailing wage withhold patterns before you chase six-figure low-slope jobs.

Audit welders, foremen, and safety leads for low-slope fluency plus equipment inventories (welding irons, hoist plans, parapet tooling) aligned to uplift and drainage clauses common in Midwest wind maps.

Clone estimating DNA: commercial spreadsheets need heavier burden for document control, bond premiums, cranes, QA photos, infrared or moisture probes, and after-hours sequencing.

Confirm Unlimited licensing timelines, indemnity wording, insurer endorsements, and bonding capacity tied to audited financial statements so municipalities stop you before boots hit the parapet.

Reliable commercial pipelines depend on disqualifying fluff before estimator mileage piles up. When your team can review fit and authority chains early, you quit donating weeks to campus walks without funded approval. Borrow intake language from the contractor growth articles we keep on the blog, then script what must be confirmed before a site measure ships.

The Illinois labor and compliance stack

Plan for Chicagoland wage pressure, union adjacency, and higher documentation loads than nearby states feel.

Illinois is not Indiana or Iowa on paper costs. Licensing friction, insurance minimums, documentation hours, and labor scarcity in the metro collar all lift burden before you add commercial retainage. Trade press out of Roofing Contractor keeps pointing at commercial labor gaps because qualified TPO welders require years, not a weekend cert, to run production pace without callbacks.

Non-union shops still need surgical efficiency to land near thirty-eight to forty-two percent gross margin when union crews anchor bid tabs downtown. Build that reality into every commercial takeoff or you will win on price and lose on execution.

Model cash without the final retainage check

"Build every commercial cash plan as if the last ten percent never arrives on time. If the job is not solvent on ninety percent of billed value, the risk to your retail float is too high."

Rebuild the acquisition mix

Facility teams in Peoria or Springfield do not respond to the same street-level tactics that fill retail routes.

The tradeoff is lifetime value: one portfolio manager can touch a dozen rooftops, so tight qualification matters more than cheap clicks.

Door hangers and yard signs rarely move a facilities director who already owns a capital plan. You need firm answers on square footage, membrane type, warranty tier, internal approval paths, and whether the contact can actually execute a contract before you load takeoff software. When the contact is only a tenant without signature power, you need to cut the thread early. LeadZik lays out plain-language notes on exclusivity, verification, and how refunds work so estimators know what they are buying into before they chase another mid-rise in Springfield.

Train on the middle step before you chase hospitals

Light commercial and multifamily are the proving ground for cash, crews, and bonding math.

How to use the light commercial bridge

Target roughly $50k to $150k envelopes so material upgrades feel real without locking up working capital the way a million-dollar tower does.

Rotate your sharpest residential leads through supervised TPO and EPDM details so field pace catches up to spec books.

Learn which owners fund through insurance events versus capital budgets so you speak CFO language and facility language in the same week.

I once watched a Metro East team vault from twenty-thousand-dollar houses straight into a $1.2M hospital wing without bonding capacity. The bid bond alone burned nearly nine thousand non-refundable dollars because their financials read residential-light. We walked them back into six-figure multifamily work for fourteen months until statements, retention reserves, and insurer endorsements looked commercial-grade. When they returned to eight-figure pursuits, the balance sheet finally matched the bravado.

Marathon pacing

Treat the commercial arm like its own P&L or the retail base that built you will pay the overdraft.

Winners run separate job costing, separate lead budgets, and separate safety cultures. One monster contract should not zero out the retail brand that kept lights on through slow hail years.

Respect the data: cash timing, production proof, documentation depth, and Illinois-specific credentials. Commercial work rewards shops that document like manufacturers, not weekend storm runners. Build that discipline and you trade storm-chase adrenaline for contracts that still pay when the radar is quiet.