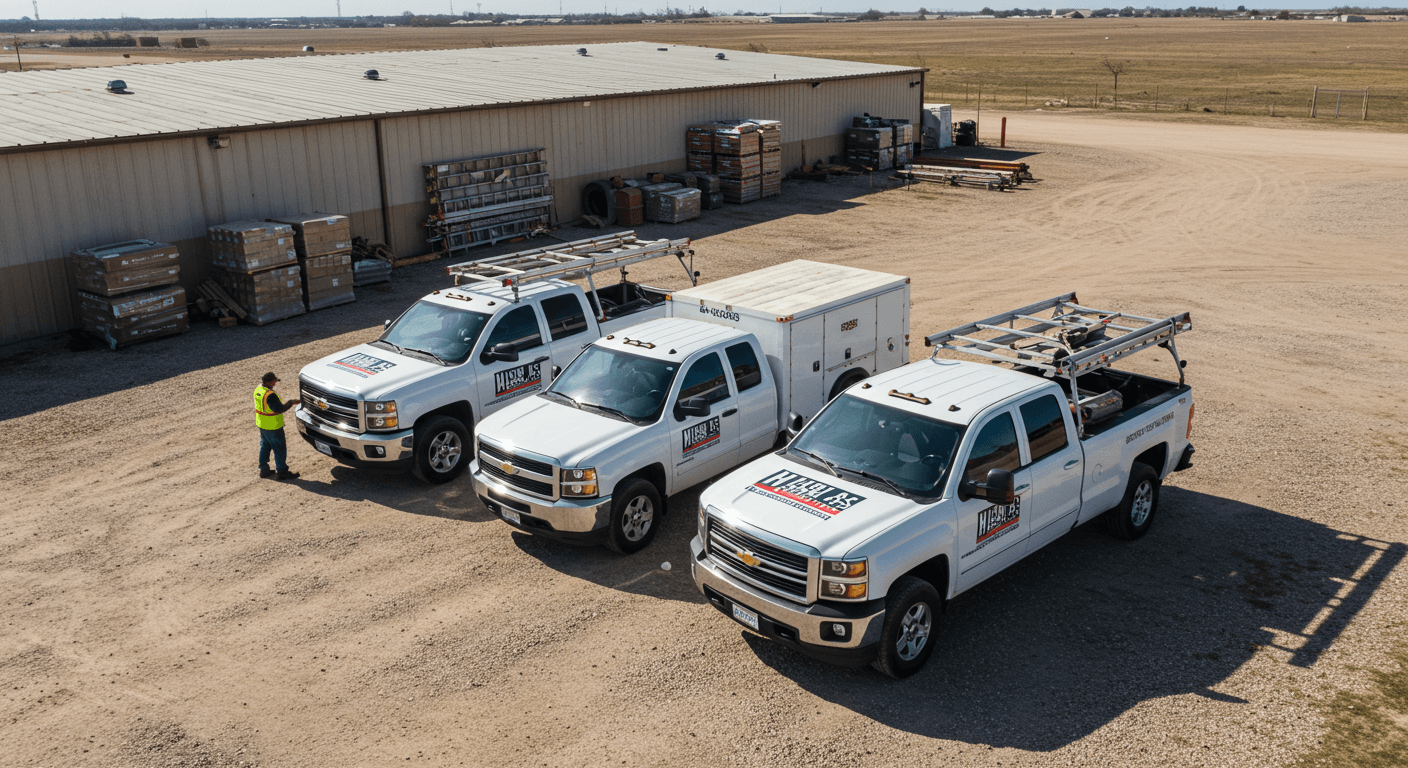

Three company trucks sat quiet in a gravel yard outside Tyler, decals weathered at the edges. Gavin traced a crease in the tailgate and quietly admitted what the spreadsheet already screamed: the rolling stock was not what he was underwriting. The durable asset was fourteen years of North Texas storm-restoration history, the referral trails, and a commercial maintenance book the seller had never priced with discipline. Revenue on the trailing statement had slipped 21.6%, yet the recurring service line pointed to steadier gross margin once somebody competent owned the pipeline. That afternoon it clicked—his next ladder for scale would not be built one canvassing route at a time. It would be bolted on through mergers and acquisitions, messy human work included.

What Operators Miss

Treat geographic density as a balance-sheet item: closer jobs shrink mobilization burn across Texas territories.

Weight recurring commercial maintenance heavier than shiny fleet photos when you normalize cash flow.

Lock scripts, safety non-negotiables, and brand standards in the first 30 days or you reopen pricing leaks.

During diligence, score cultural fit before you fall in love with depreciated equipment.

Average bump we track when a roofing platform absorbs a second Texas region and fully integrates ops inside eighteen months—not headline revenue, but how buyers pay.

Texas is ground zero for tuck-in deals. Private equity scouts and aggressive owner-operators are stalking the I-35 spine, while Gulf-adjacent rebuild cycles keep balance sheets strained and sellers open to talks. If you are parked around $4.2M in sales and bumping the ceiling, buying a peer is rarely “just more crews.” You are buying map coverage, estimator talent, and the right to argue for a higher EBITDA multiple once the platform looks replicable. A lone shop might clear 3.2x normalized earnings; a multi-region Texas operator running one finance stack and one safety doctrine can justify 5.8x or better when the story is documented.

Reading the Texas map before you wire earnest money

Not every acquisition thesis travels west to east. Match the market phase to your risk tolerance.

Dallas–Fort Worth is crowded—organic customer acquisition is expensive, so deals often buy labor specialization and instant share. Conversely, the Austin–San Antonio corridor is expanding fast enough that hesitation means paying industrial rent you refused six quarters ago. Last month I challenged an owner eyeing Lubbock: the rigs were tired, but an 8.4% local share in a county where his flag was invisible was worth more than fresh vinyl wraps. In Texas, longevity still converts; a nineteen-year storefront brand transfers trust faster than a year of billboards.

Model the storm-season lag. A book that is 94% hail-reactive wobbles when spring stays mild. You want maintenance, retail, and light commercial to flatten the curve, and you want proof the team can prospect through blue skies. Shops still leaning on yellow-pages nostalgia are mispriced targets if you layer modern prospecting—study how contractors diversify inbound work in guides like this overview of roofing lead tactics from IKO—then stress-test whether you can replicate that playbook post-close.

Normalize the numbers before you romanticize the logo

EBITDA tells the truth; owners often tell the fable.

Sellers love anchoring on revenue multiples. Buyers live in EBITDA and quality-of-earnings work. During Gavin's management workshop we surfaced an owner-heavy referral base—roughly 43% of word-of-mouth revenue looked likely to walk if the founder ghosted. That risk directly trimmed our valuation band. Strip the add-backs next: personal trucks, beach “retreats,” family phones. I have seen shops reporting breakeven operating income reveal 14.8% net margin once the lifestyle expenses are carved out.

The 90-day ghost rule

"Keep the seller in a consulting role for ninety days only—long enough to transfer relationships, short enough that they cannot veto your new production standards."

Inherited liability travels farther than goodwill

Safety debt is balance-sheet debt. If crews treated harnesses as optional yesterday, you may absorb OSHA exposure that outlasts the transaction premium—audit like the fines hit your personal account.

Treat regulatory exposure like deferred maintenance on a membrane roof—you pay eventually. Cross-check incident logs against OSHA's roofing compliance expectations before you inherit someone else's supervisory gaps. I toured a Houston property with a buyer once; inside ten minutes we spotted three installers working steep-slope without fall protection. We passed. Six months later that shop faced a six-figure enforcement action—exactly the sort of tail risk that deletes merger IRR.

Pressure-test lead economics with the same skepticism. Shared, rotated prospects closing at 7.2% tell you the pipeline is malnourished, not “efficient.” Replacing feast-or-famine chaos with consistent intake is where platforms shine—browse our playbooks on roofing growth and lead strategy when you need language to explain the upside to lenders and integration teams.

Asset purchase versus stock purchase

| Decision factor | Asset purchase | Stock purchase |

|---|---|---|

| Liability firewall | Buyer usually leaves most unknown liabilities with seller | Entity-level lawsuits and tax issues can transfer |

| Contract continuity | May need assignments or novations on key agreements | Existing contracts often remain in force |

| Tax basis step-up | Potential to step up certain asset values | Limited step-up benefits versus asset deal |

| What you cherry-pick | Select fleets, tools, customer lists, and IP | Acquire entire operating shell, warts and all |

Liability firewall

Contract continuity

Tax basis step-up

What you cherry-pick

Work with Texas counsel—choice of entity, lien law, and license continuity will swing the practical answer even when the spreadsheet whispers stock.

Merge sales cultures without starting a civil war

Technique matters more than cheerleading when two brands share one forecast.

Failed integrations usually trace to tribal sales behavior, not shingles. One crew may still close on emotion at the door; another leans on aerial measurements and tablet presentations. When Gavin combined rosters, resentment spiked until we forced overlap instead of speeches. We opened with a single homeowner-facing narrative—your prospect does not care whose embroidery is on the shirt; they care if you can steer a $28,740 insurance scope without wasting their weekend.

A structured shadow week let veterans trade strengths: the acquired reps articulated shingle-tier durability with precision, while Gavin's original closers compressed decisions on first visits. Blending those behaviors lifted average contract value 11.2% in sixty-four days. If pipeline volume suddenly outpaces training bandwidth, revisit how you source demand—our FAQ on exclusivity and lead quality helps you ensure reps are not burning hours on recycled names.

Action Plan

Operational mesh after the champagne bottle pops

Fleet integration is more than magnetic signage. Treat dispatch, fuel, and vendor tiering as immediate EBITDA levers—not Phase IV projects.

Centralize scheduling so Denton and Fort Worth crews stop crossing routes for material pickups.

Negotiate shingle and accessory rebates using combined square volume; aim for mid-single-digit savings that fall straight through.

Benchmark fuel and windshield time weekly; we cut fuel spend 9.3% in five months once hubs were obvious.

Document SOPs for warranty and supplement escalations so acquired PMs do not invent their own chaos.

Build for the institutional exit—even if you never sell

Discipline that attracts PE also makes the business survivable if you stay in the chair.

Acquisitions are too painful for a slightly larger truck payment. They earn their keep when you are constructing a platform someone else can underwrite: leadership that survives without the founder, diversified intake across referrals, digital, and vetted external partnerships, standardized workflows, and proof of performance across more than one MSA. Buyers stopped paying premiums for heroic owner-operators years ago—they pay for predictable cash conversion.

Gavin's north star is not a vanity revenue headline. It is durable 22.7% year-over-year growth with defensible share across the markets he assembled. That is the difference between selling a job and selling an enterprise.