$24,672 in annual interest and depreciation leaks from the average Colorado roofing fleet for every three-quarter-ton truck that clocks fewer than 11,400 miles per year. This capital drag is getting louder as borrowing costs for specialized gear, steep-slope shingle lifts, high-capacity dump trailers, and similar tools have climbed by nearly 42% over the last 34 months. Denver and Colorado Springs are splitting into two camps: shops carrying heavy debt on the balance sheet, and owners moving toward lighter, on-demand equipment plans. The point is not shaving a payment for its own sake. It is keeping cash available when winter slows the funnel across the Front Range.

While one side of the market is buried in fixed overhead, more systematic owners use utilization math to choose finance versus rent. Owning a specialized $68,432 asset that only deploys on 14.5% of jobs is an operational anchor. In markets like Fort Collins, insurance claim cycles can lag for weeks, so a lean debt-to-equity position is often what separates scaling from a rough quarter.

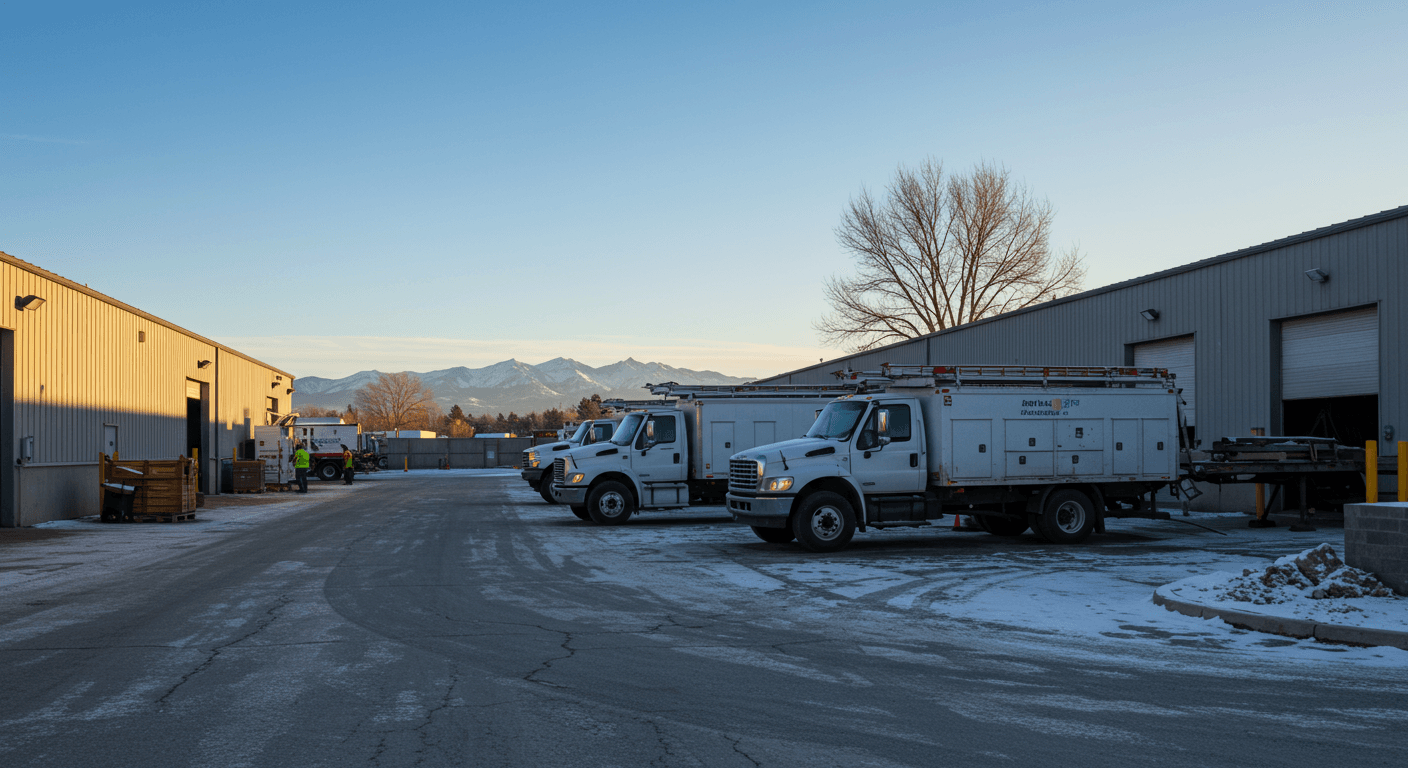

Fleet ROI on the Front Range

If specialized gear is not on a job site at least 23 days per quarter, renting usually beats financing once you add interest, insurance, and storage.

High-rate vehicle notes can shrink the credit line you need for large material buys when hail season spikes demand.

Mountain grades and road treatment accelerate wear; plan depreciation about 12% faster than national averages when you model payments.

Match fleet capacity to work you can actually book so financed assets earn hours instead of sitting behind the shop fence.

The pull of a polished fleet

New trucks look sharp on the street. The ledger tells a different story when utilization is soft.

I worked with an owner in Aurora, call him Xavier, who believed ten brand-new wrapped trucks were his best billboard. On paper, the image was strong. In the books, those trucks were running about $9,430 a month in payments and insurance before fuel. When we mapped real dispatch, two rigs sat in the yard roughly 68% of the time.

He was paying for capacity the sales calendar could not feed. Storm markets encourage that instinct, but financing for peak weeks while you live on base volume is how cash gets thin fast. Reporting from Roofing Contractor lines up with what I see in the field: debt discipline matters as much as crew skill when revenue swings hard.

Blended from recent P&L reviews with Colorado roofing shops where trucks and trailers carried full notes but utilization stayed under the 22% revenue-day threshold.

The 22% rule: finance or rent

If the asset does not earn calendar days, the note wins.

The decision to finance a new Equipter row or a line of F-250s should be boring math. I use a 22% utilization threshold. If you cannot place a piece of equipment on a paying job for at least 22% of workable days in a year (about 55 days once you discount Colorado weather), interest and insurance tend to outrun short-term rental.

Here is a clean dump trailer example. Purchase price near $14,850. At current rates, a monthly payment might land around $315. Add $110 for insurance and $45 for maintenance and tires. You are near $470 a month. Twice-a-month use for small repairs makes the cost per pull about $235. A commercial rental might be $115 for the day. Financing can double the per-use cost when utilization is thin.

Dump trailer: own versus rent at low utilization

| Cost factor | Finance (2 uses / mo) | Rent (2 days / mo) |

|---|---|---|

| Monthly cash out | ~$470 loaded (note, insurance, upkeep) | ~$230 (2 x $115 day rate) |

| Cost per use | ~$235 | ~$115 |

| Balance sheet | Depreciation + debt on the books | Expense only, easier to flex down |

Monthly cash out

Cost per use

Balance sheet

The Colorado registration bite

Colorado ownership tax ties to original MSRP. Financing a $74,000 truck can push annual registration well above a $48,000 used unit, even when the monthly payment feels fine. Plan for that extra drag on vehicle ROI in the first three years.

Storm season scale without a five-year hangover

Peak hail is temporary. Long notes are not.

When hail tracks across the Front Range, the reflex is to finance everything for three new crews. Storm seasons are short. A five-year note written for a two-year weather window is a classic path to distress. Operational leases, rental partners, or subcontracted haul-off can keep fixed costs closer to actual demand. Shrink the monthly minimum you need to survive so deep snow weeks do not decide your payroll.

Pipeline clarity matters here. If your team uses the LeadZik mobile app to claim work as soon as it is live, you can see demand forming before you add another trailer payment. If next week looks light, you pause the capital decision instead of reacting after the fact.

Altitude, salt, and realistic loan length

A truck can be tired before the note is gone.

Colorado is hard on equipment. High passes and magnesium chloride on I-25 age suspensions, brakes, and cooling systems faster than a truck that lives on coastal flats. If you finance like the asset will last 72 months but the rig is spent at 48, you risk being upside down with a repair bill waiting at the worst moment. I steer owners toward 36- to 48-month structures on primary roofing vehicles. If the 48-month payment does not fit, the spec is usually wrong.

Technical guidance from the National Roofing Contractors Association (NRCA) keeps reinforcing reliability and safety. A breakdown on the way to a Vail steep job costs labor hours and reputation faster than a slightly higher payment on a truck that actually starts.

The 1.5x maintenance reserve

"In Colorado, fund maintenance at about 1.5x what you would use in a milder state. Steep grades and wide temperature swings chew through brakes, transmissions, and cooling systems sooner than book averages suggest."

Align leads with the assets you are financing

Expensive steel should chase work that needs it.

Every day a financed truck sits, active jobs subsidize that idle cost. The fix is predictable work that fits the fleet you already carry. Shops gain margin when they stop sending steep-slope crews with hoist systems into flat work that never needed that capital stack.

On LeadZik, you can review job details and photos before you purchase a lead, which makes it easier to send your highest-cost assets to scopes that actually pay for the note.

Action Plan

Five-step fleet finance audit

A simple quarterly pass to spot equipment that is earning its keep versus equipment that is quietly eating margin.

Calculate daily carry: add monthly payment, insurance, average maintenance, and yard storage for each unit, then divide by 30.

Pull utilization from GPS or dispatch logs: count days each vehicle actually leaves for a paying job.

Map job type to gross profit: flag routes where an expensive diesel rig supports a low-dollar ticket.

Price rentals quarterly: call a commercial rental house for the trailers and lifts you use least.

Sell or sub out anything under 22% utilization for six months and shift those scopes to rent or partner labor.

Financing as a tool, not a flex

The Colorado shops I respect carry cash, not just chrome. Treat every vehicle purchase like a capital project with a utilization forecast, not a morale boost. Keep debt tied to assets that move production, pair that discipline with steady job flow, and net margin starts to reflect the work your crews actually perform.